#

#

Pine Labs Online

Agent commerce, built for banks

A briefing for business and risk leadership, with a working demonstration.

PINE LABS ONLINE

01 / 15

#

02 · Context

Agents are starting to buy

Technology used to help a customer decide. An AI agent now completes the purchase itself, on an instruction given once, inside a budget set in advance.

53%

of web traffic is now automated. A signal of how fast automation is rising, not proof that agents are already buying. The share was 50 percent in 2023 and 51 percent in 2024.

Human searches, human pays.

The customer finds it and buys it. Traditional commerce.

The agent searches, the human pays.

The agent narrows the options, the customer still pays. Where the market is now.

The human searches, the agent pays.

The customer chooses, the agent completes the payment. Emerging.

The agent searches, the agent pays.

Both sides run without a person in the loop. The full shift.

Every one of these purchases still needs an identity the customer's side and the merchant's side both trust. Holding that identity has always been a bank's work.

Thales / Imperva Bad Bot Reports, 2024 to 2026 editions. Automated traffic includes both benign and malicious systems.

PINE LABS ONLINE

02 / 15

#

03 · What we offer

Agent commerce on the bank's own rails, under the bank's control

Pine Labs Online is a single layer that lets AI agents buy and sell across the bank's own merchants and rails. Every agent carries an identity, a limit and a record the bank issues and can revoke, and nothing settles outside the institution.

Grantex.

Agent identity, permissions and spending limits, controlled by the bank.

OACP.

One connection to every payment protocol, P3P live inside it.

The bank's rails and merchants.

Settlement and supply that never leave the institution.

What the bank gets

Own the marketplace.

The bank's merchants become a surface agents buy from, under its name.

Keep the relationship.

Every search, purchase and mandate runs through the bank, and the data stays with it.

Provable control.

An identity, a limit and a signed record behind every action, ready for the risk team.

Nothing new to build.

It runs on the acquiring, rails and merchants already in place.

PINE LABS ONLINE

03 / 15

#

04 · Opportunity

The bank already holds most of what this needs

The parts that take years to assemble are the parts a bank already holds. A large merchant base supplies the goods. Established rails move and reconcile the money. Direct customer relationships carry the trust a purchase rests on. What the market still lacks is one layer that lets automated buying work across all three, safely and under a single authority. That layer is what Pine Labs Online adds, and it is the fast part, because everything beneath it is already running.

Already held by the institution

A merchant base. One of the largest in the country. The supply side is already there.

Settlement rails. Money already moves and reconciles through the institution at scale, every day.

Customer relationships, identity and KYC. The direct trust a purchase depends on, and the identity the bank already issues and verifies, are all in place.

Added by Pine Labs Online

Agent identity and limits. The bank issues each buyer or seller agent an identity it can check, a spending limit, and a record open to inspection. The customer's own identity stays where it is.

Both sides represented. An agent that buys for the customer, and an agent that presents the merchant. Both run under rules the bank sets.

A single point of control. One authority across merchants, rails and relationships.

The bank already owns identity. What is new is issuing that identity to the agent, and Grantex is how it is issued and governed.

PINE LABS ONLINE

04 / 15

#

05 · Control

Grantex governs every agent, from issue to revocation

This is the first of the two capabilities that make everything else possible, and the one a risk team will look at hardest. Before any agent spends a rupee, it has to establish who it is and what it has been allowed to do. Grantex does that for every participant, without exception. It issues each one a checkable agent identity and a fixed set of permissions, then verifies both at the moment of action, before anything runs. It sits at the centre of the whole arrangement. Every request passes through it. None goes around it.

The full life of an agent: registered, identity issued, permissions granted, every action checked in scope, audited and revocable at any moment. A child agent can never exceed its parent.

A compromised participant still cannot exceed the authority it was given, because that authority is enforced at the point of action, not trusted to good behaviour. Everything that follows rests on this.

GRANTEX

Identity.

Every participant carries an identity that can be proven. Nothing anonymous gets in.

Permissions.

The exact set of actions allowed, and nothing past it. Set by the institution.

Spending limit.

A ceiling on amount, purpose and duration, checked before each action.

Record.

A permanent log that cannot be altered after the fact. One answer to who authorised any action.

PINE LABS ONLINE

05 / 15

#

06 · The money

Money moves only on rails the bank already runs

With control established, the next question is the money itself, and it is the one a risk team asks first. The system assembles the evidence for a purchase and executes the payment when the mandate's conditions are met. This is timing and execution inside a pre-authorised mandate, never a credit decision. Moving the money is one step in that chain, and it happens on the institution's existing rail exactly as it does for any transaction today. No new instrument. Nothing held or settled outside the bank at any point.

Net banking

The agent pays from the customer's own account on the institution's net banking rail, inside a mandate the customer approved once.

UPI mandate

For smaller, recurring amounts, a sum is reserved upfront and drawn against as conditions are met, under a single approval and within NPCI's own mandate rules. This is the rail P3P runs on in production today.

Cards

Where a card is the right instrument, the transaction runs inside the same authorisation the institution operates for card payments today.

Whichever rail carries it, it stays the institution's rail. The economics stay as they are today, and control of the funds never passes elsewhere.

A live mandate on the UPI rail: limits enforced, one debit when the condition is met, settlement on the institution's side.

PINE LABS ONLINE

06 / 15

#

07 · Reach

One connection reaches every payment protocol

New standards for automated commerce keep arriving. P3P, Pine Labs Online's own protocol, is live on UPI today; the card networks follow on the roadmap. Without a shared layer each one is a separate integration, contract and record. With OACP the institution connects once, and its merchants are reachable across all of them, including the ones that arrive later.

Today

MERCHANT

P3P

Mastercard

Visa

UPI

Four integrations, four contracts, four records.

With OACP

MERCHANT

OACP

P3P · LIVE

Mastercard

Visa

UPI

Whatever follows

One connection. Every standard, including the ones that arrive later. P3P is live; the card networks are on the roadmap.

One integration in place of four.

Each new standard is connected a single time, on the Pine Labs Online side, and every merchant is carried across automatically.

A live protocol already inside it.

P3P is not a future item. It is Pine Labs Online's own protocol, running in production inside OACP today.

The pattern has a precedent.

Merchants once ran a separate gateway for every bank. Aggregators collapsed that into one and led the category for a decade. This is the same move, on automated commerce.

Deployment is two components inside the bank, with OACP as the one connection outward; nothing else in the stack changes. And the same principle holds for discovery: one catalogue entry reaches every customer-facing surface, covered shortly.

PINE LABS ONLINE

07 / 15

#

08 · From assistant to settlement

A purchase can start in ChatGPT and still settle on the bank's rail

Customers are already asking assistants to buy. When they do, the request routes onto the bank's rails rather than around them.

Outside the bank

The assistant surface

ChatGPT, Claude, or whatever follows. The customer asks it to buy.

→

Inside the bank

The buyer agent

Carries the customer's mandate, identity and limits, issued through Grantex.

→

The agentic marketplace

Finds it across the bank's own merchants, from the confirmed catalogue.

→

Settlement

One debit on the bank's rail. Nothing held or settled outside.

The origin can sit anywhere. Execution and settlement stay inside the institution.

PINE LABS ONLINE

08 / 15

#

09 · The agentic marketplace

Your merchants become a marketplace agents buy from

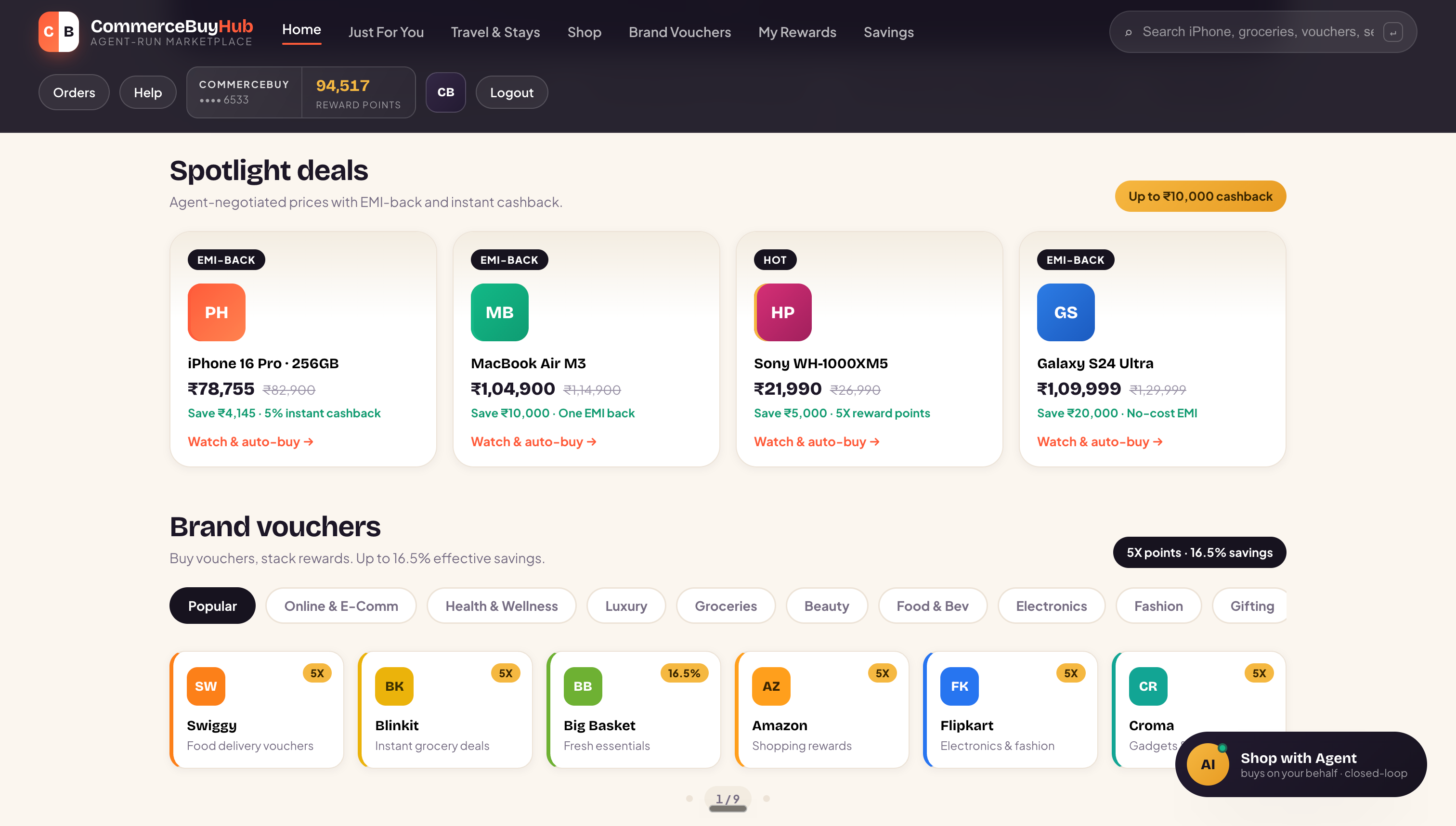

A customer says what is wanted and sets the conditions. The agent finds it across those merchants and completes the purchase inside the limits set, without a person attending each step. The merchant keeps its own brand and its own commercial terms, and gains reach it could not build alone.

The bank's merchants, under the bank's name.

A surface made up entirely of merchants who already bank there. Not a third-party marketplace.

Buying without constant attention.

A customer sets a rule once. The purchase proceeds when the conditions are met, at any hour, inside the agreed limits.

Full visibility kept.

Every search, purchase and mandate runs through the institution. The relationship and the data stay with it.

Found on every surface, from one catalogue entry.

Retrieval runs over a catalogue the bank controls, not the open web. As each assistant surface appears, Pine Labs connects it; the merchant never integrates again.

The bank's merchants become a place agents buy from, under the bank's name.

The merchant base shown as one surface, under the bank's own name: agent-negotiated prices, watch-and-auto-buy on every item. Live proof: Vijay Sales, flash-sale pre-authorisation on P3P.

PINE LABS ONLINE

09 / 15

#

10 · In production

Live today with Gullak and Vijay Sales

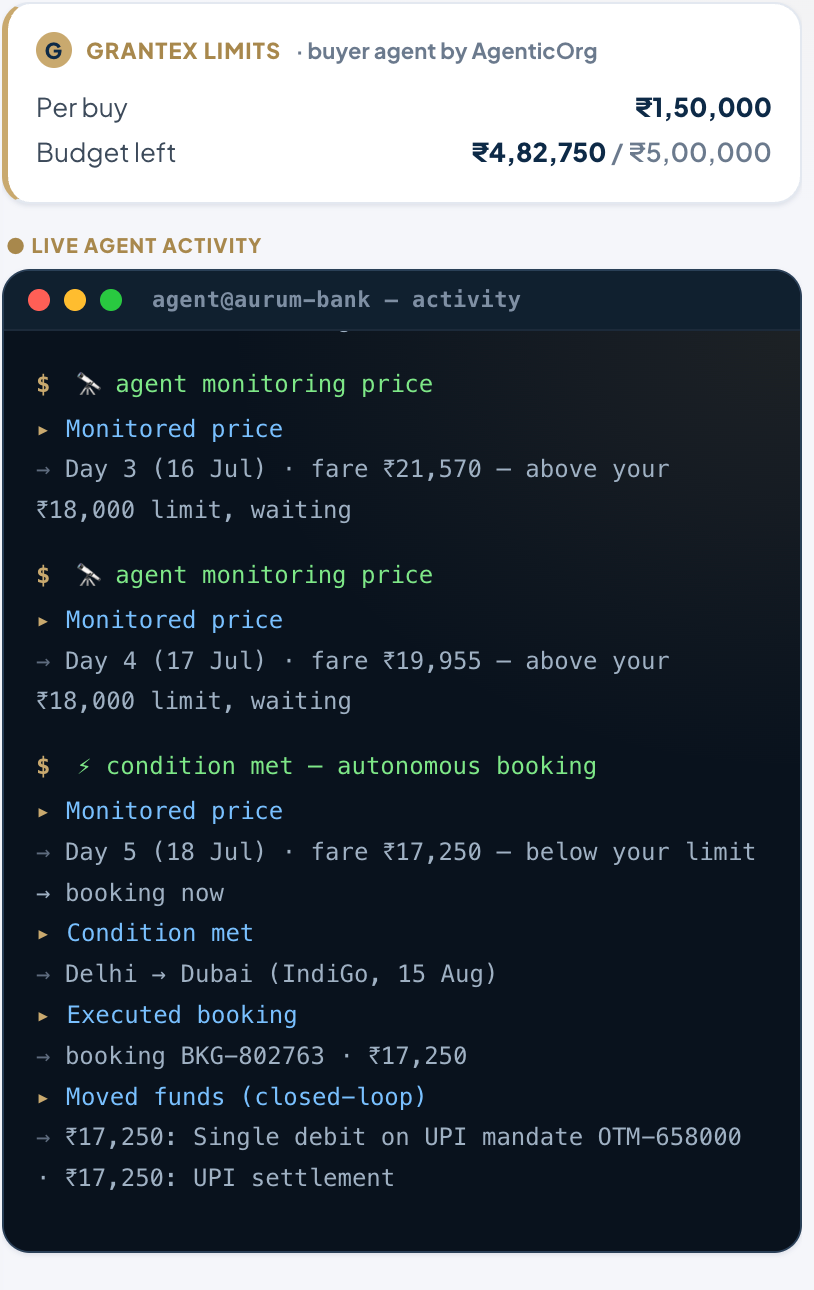

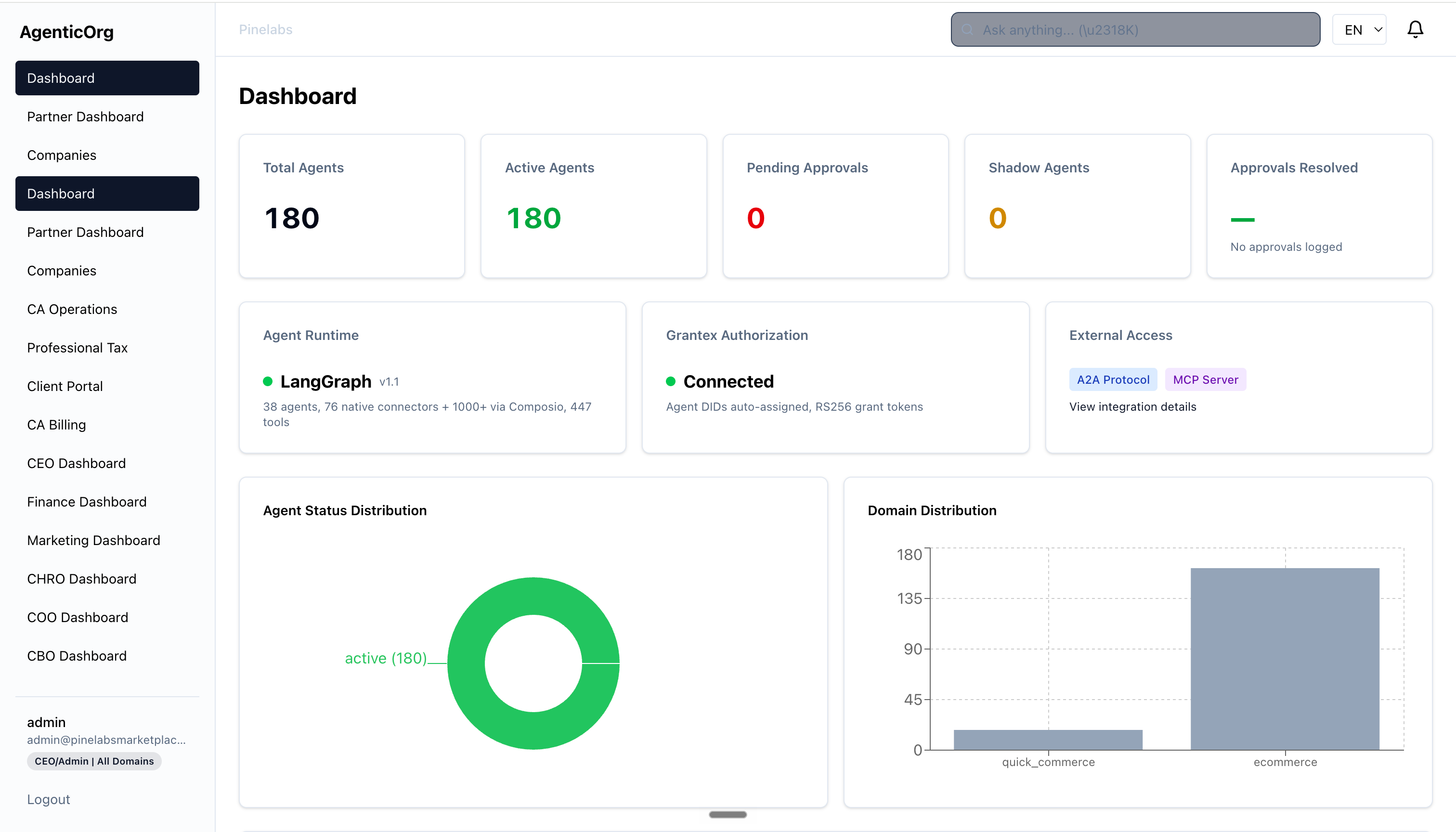

This runs in production now, not on a roadmap. P3P, the protocol described earlier, operates today on UPI mandate rails. Two deployments are live on it. The first buys gold on a rule the customer sets, running with Gullak, and completes the purchase the moment the price condition is met. The second reserves and secures an order during a flash sale, ahead of the crowd, running with Vijay Sales. The console below is where an institution supervises all of it, with every participant's identity, permitted actions and spending limit in one view.

Live participants.

Each carries a verified identity and a spending limit.

Grantex, connected.

Identities signed, authorisations issued.

Nothing outstanding.

No participant acting beyond what it was approved to do.

Live deployments with Gullak and Vijay Sales, on P3P over UPI mandate rails. Console figures are from a working deployment.

PINE LABS ONLINE

10 / 15

#

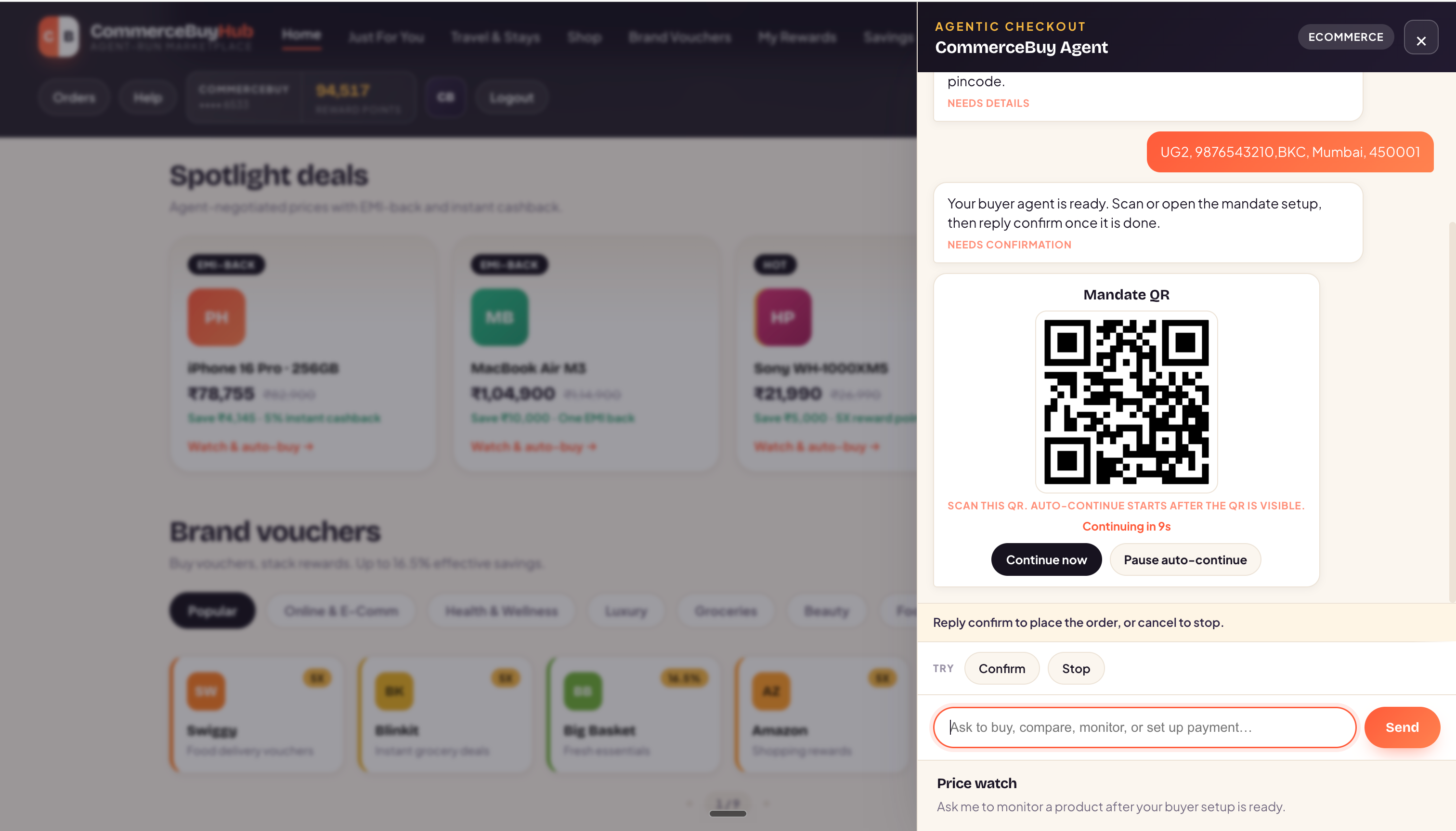

11 · Net banking

One approval, then the agent buys inside the limit

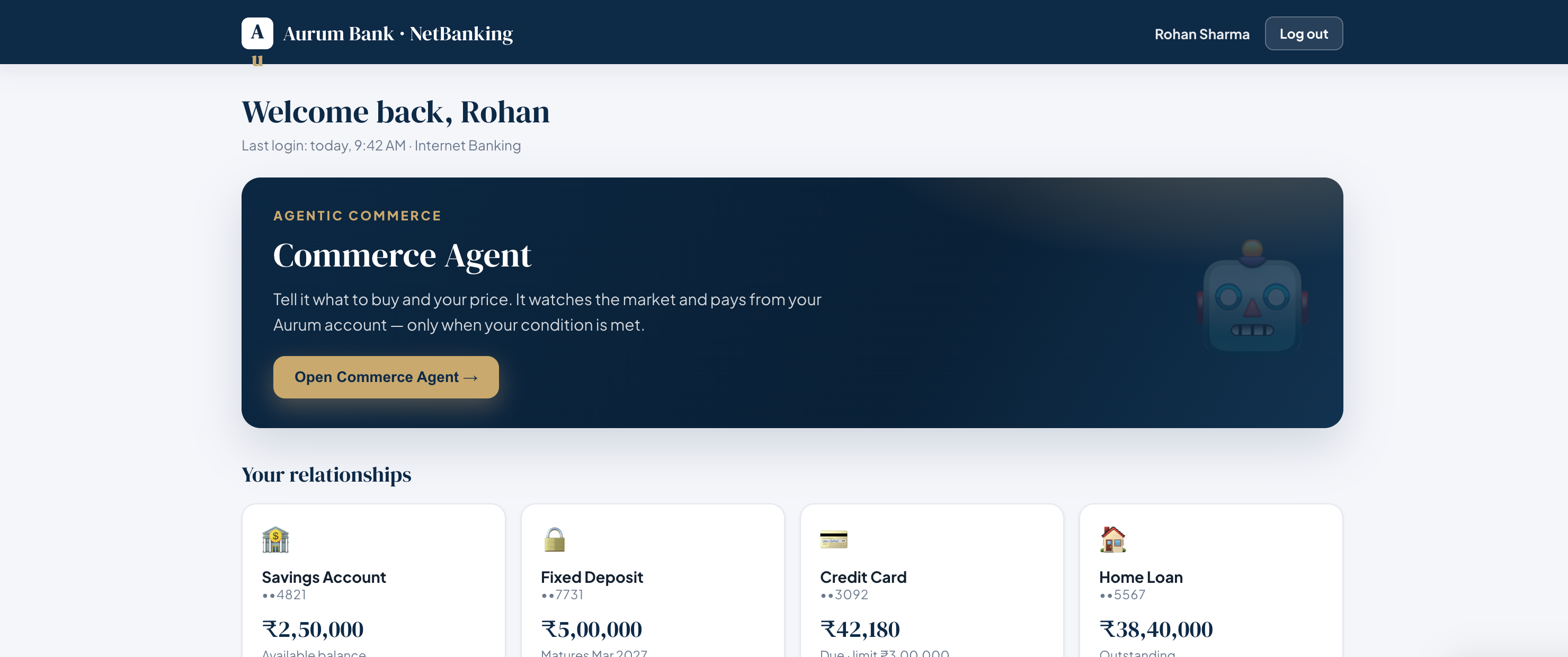

You have seen that it is live. Here is one purchase, end to end. The customer opens net banking, sets a limit, approves once, and leaves it to run. The agent watches conditions, waits until they are met, buys inside the ceiling, and closes the mandate.

It starts inside net banking, under the bank's own name. Live proof on this flow: Gullak, buying gold on a customer's rule.

The agent buys inside that storefront: address confirmed, UPI mandate approved, order placed in one thread.

It starts at the bank.

The customer opens net banking and starts a buying session.

The limits get set.

A ceiling per purchase and in total, granted and enforced through Grantex.

One approval, upfront.

A single mandate, approved once, and the agent is cleared to act.

It buys, then stops.

Days of watching, one debit when the price drops, mandate closed.

Every step ran inside limits the customer set one time, and the institution saw all of it.

Working prototype. Merchants and amounts shown are illustrative.

PINE LABS ONLINE

11 / 15

#

12 · Why Pine Labs

The hard parts are already built and carrying real volume

Why Pine Labs rather than anyone else who could draw the same architecture? Because the hard, slow parts are already built and carrying real volume.

980,000+

merchants on Pine Labs

6 billion+

transactions processed

₹11.4 trillion

settled through the platform

The scale is already here.

Automated commerce is added on top of a base already at this size, not built up to it. Figures are cumulative across the platform.

The protocol is live, not proposed.

P3P is running in production today on UPI mandate rails, with two merchant deployments already operating on it. Most of the market is still describing what it intends to build.

The agent-identity layer already exists.

Grantex is built code, not a specification, mapped to SOC 2 criteria and released under an open licence. The control model in this deck is running, not sketched.

The merchant complexity is already understood.

Thousands of merchants onboarded across the storefront and ERP systems these stores actually use. Connecting a real merchant is known ground here.

Very few already own the rails it settles on, the merchants it reaches, and a live protocol running across both.

Platform figures are cumulative across Pine Labs. P3P is live on UPI mandate rails; card and other rails are on the roadmap. Grantex controls are mapped to SOC 2 criteria.

PINE LABS ONLINE

12 / 15

#

13 · The proposition

Begin with one scoped pilot

The way in is deliberately narrow: one defined pilot, with success agreed before anyone builds, and the risk function in the room early, because the control model is the point.

Grantex.

The control layer every participant runs through.

OACP.

One connection to every current and future protocol, P3P already live within it.

Existing rails.

Settlement that never leaves the institution.

The merchant surface.

The bank's own merchants, under its own name, found across every surface.

Provable control.

A checkable basis for every action.

Three steps to begin

A joint working session.

Business and technology leads in one room, on the use cases that fit the institution's book.

The risk function, early.

A direct review of the controls, the lifecycle and the means of suspension. Its confidence is what opens the path.

A scoped first pilot.

One merchant group, one category, one rail, with the definition of success agreed before any build starts.

What the pilot delivers: a working agent purchase on one of the bank's own rails, with a success metric agreed upfront and a result in weeks, not quarters.

PINE LABS ONLINE

13 / 15

#

#

The next move

Put the first pilot on your own rails

One category, one rail, success defined before anyone builds. The market is forming now, and the institution that moves first is the one the others follow.

Start here

A working session with business, technology and risk in one room, to scope that first pilot.

Pine Labs Online

A briefing for business and risk leadership

A briefing for business and risk leadership

14 / 15

#

15 · Appendix

Built to the expectations in RBI's FREE-AI framework

RBI's FREE-AI framework sets out the expectations for responsible AI in the financial sector. Every expectation it names already has a home in this architecture, and most of them map directly onto the identity lifecycle shown earlier. The full mapping is below.

FREE-AI expectation

Corresponding element

Human oversight

Approval workflows and escalation

Governance of third-party AI

A registry of participant identities

Continuous monitoring

Ongoing telemetry and observation

Suspension and retirement

Immediate disablement, with a parent able to revoke those beneath it

Explainability

Decision logs and a full reasoning trace

Accountability

Signed records of every action

Vendor governance

Enforcement of identity and permitted actions

Customer disclosure

The participant's identity shown to the customer

RBI, Framework for Responsible and Ethical Enablement of AI, 13 August 2025. Advisory, not binding. Architecture designed to these expectations. Rollout staged.

PINE LABS ONLINE

15 / 15